With multiple banks and credit unions competing for the same member relationships, retention is no longer just about loyalty, it is about sustainability and long-term growth. According to JD Power, credit union member satisfaction declined in 2026, while more members quietly expanded relationships with other institutions. In fact:

- 59% of members now maintain checking accounts elsewhere

- 56% hold savings accounts outside their primary institution

This signals a shift toward “soft switching,” where members do not formally leave but gradually reduce engagement. The National Credit Union Administration further highlights the urgency, noting that in 2025, over 55% of credit unions experienced a decline in membership, making it increasingly clear that understanding and addressing member disengagement must now be a top strategic priority for credit unions.

Why It Matters: Disengagement Is a Process, Not an Event

Member attrition rarely happens suddenly; it develops over time through subtle behavioral changes. In a relationship-driven model, value is built continuously, which also means it erodes gradually if not actively managed. Early signs of disengagement often include:

- Fewer digital logins

- Declining balances

- Reduced transaction activity

- Dormant credit cards

- Loans paid off without follow-on engagement

Individually, these signals may appear minor, but together they set a narrative for a weakening relationship.

The challenge is that most credit unions view these behaviors in silos, often relying on backward-looking reports focused on past activity rather than emerging risk. Based on the traditional reporting, many institutions are able to see what changed but still struggle to determine:

- Why it changed

- Whether it is meaningful

- What action to take

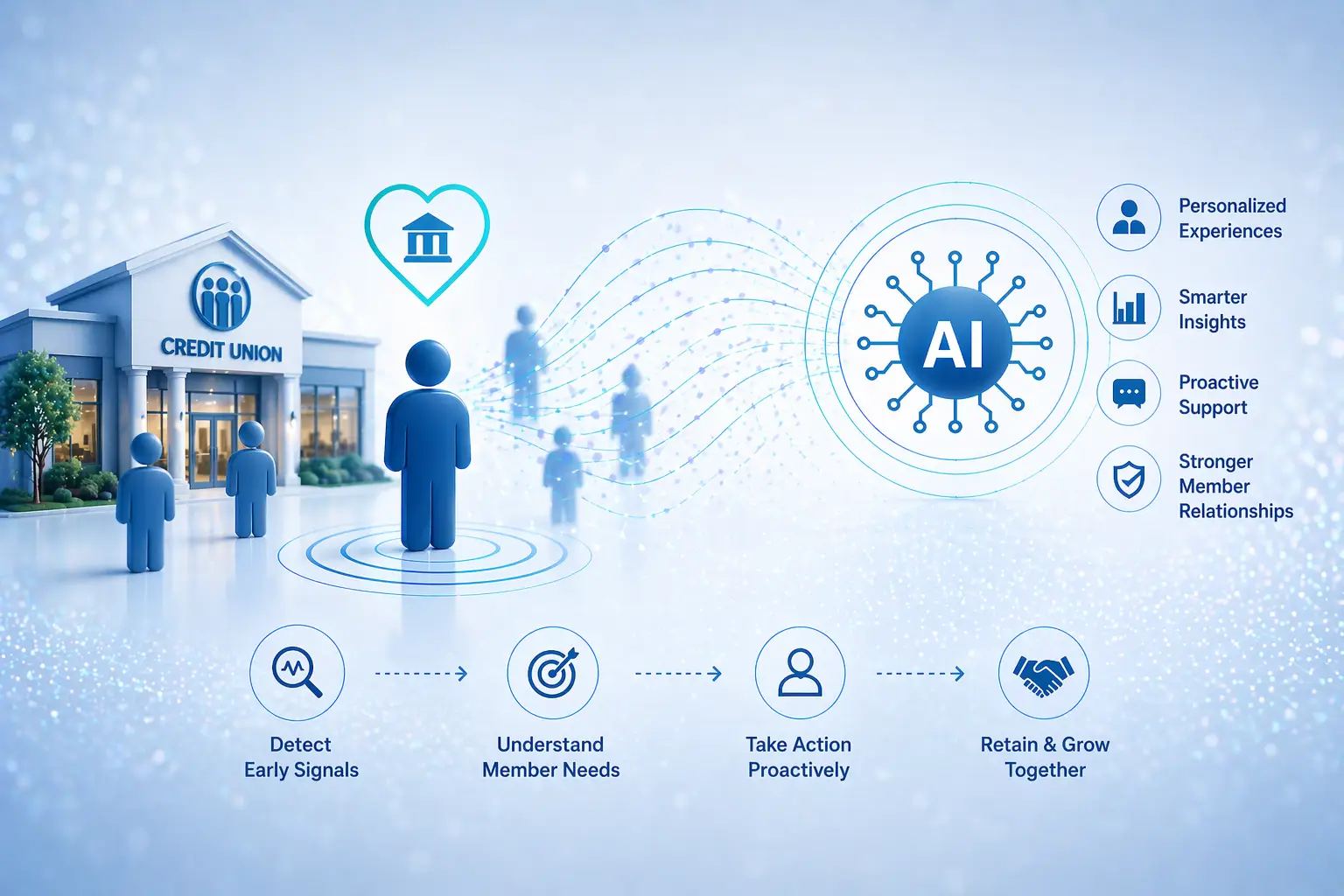

What Is Happening: AI Connects the Dots

This is where AI introduces a far more connected predictive approach to understanding member behavior by bringing together signals that would otherwise remain isolated.

Disengagement is rarely obvious when viewed through a single lens, and individual indicators often appear too small to warrant action; however, when analyzed collectively, they reveal patterns that tell a much more complete story.

By layering AI into this process, credit unions can shift their focus from retrospective analysis to forward-looking insight, enabling them to move beyond asking why a member was lost and instead focus on:

- Which members are showing early signs of disengagement

- What specific behaviors are driving that risk

- What actions can be taken immediately

AI models can detect risk 3–9 months before churn, creating a valuable window to act.

Modern AI capabilities extend beyond prediction to explanation, translating complex data into clear, human-readable insights. Instead of relying on abstract risk scores, often difficult to interpret, credit unions gain clarity through:

- Plain-English explanations

- Key drivers behind disengagement

- Full relationship context across products

So instead of saying Risk score of a member is 6, it tells that the member is classified as “medium risk” because they maintain strong checking activity but show declining engagement in savings and credit card usage. This level of transparency makes insights actionable for frontline teams, not just analysts.

How to Act: From Insight to Real Engagement

Once credit unions understand both the “what” and the “why,” they can shift from reactive outreach to proactive engagement. This allows for:

- Timely interventions aligned with member behavior

- Personalized offers based on actual needs

- Early re-engagement before relationships weaken further

This shift is critical as member expectations are increasingly shaped by seamless digital experiences. It also transforms how different credit union teams operate:

- Marketing: Moves from broad segmentation to behavior-driven precision

- Member Experience: Evolves from reactive service to proactive engagement

- Leadership: Shifts from reporting outcomes to influencing them

Adopting a predictive approach does not require an immediate, large-scale transformation, but it does require a focused and structured starting point that builds momentum over time. Credit unions can begin by:

- Identifying member segments showing early disengagement signals

- Applying predictive models to assess and quantify risk

- Launching targeted, personalized engagement strategies

- Measuring outcomes and refining approaches continuously

Over time, this evolves into:

- A self-improving retention engine

- More accurate risk identification

- Stronger and more consistent member engagement

The Bottom Line

Credit unions are not losing members overnight, but through a gradual decline in engagement and missed early signals. The institutions that will succeed are those that can answer early and accurately what is happening, why it is happening, and how to act. Because the future of member retention is not reactive but predictive & proactive, and those that make this shift will build stronger, more resilient member relationships in an increasingly competitive landscape.

If you are a credit union looking to arrest member attrition and disengagement early, reach out to the AiVantage team today to leverage predictive intelligence and drive meaningful, personalized engagement.