This article was originally published on CUInsight. Read the full article Here.

Over the past decade, the financial services industry—banks, credit unions, and fintechs—has invested heavily in predictive analytics. From credit scoring and underwriting to fraud detection and customer segmentation, predictive models now power critical decisions.

The numbers reflect that maturity. More than 70% of large banks rely on predictive models for credit and risk decisioning, while fraud systems analyze millions of transactions per second globally.

But here’s the real question: if prediction is so advanced, why does action still feel slow, manual, and inconsistent? A system can flag a risky transaction. It can identify a customer about to churn. It can surface a high-probability cross-sell opportunity.

And yet what happens next? Nothing—the system waits on us.

The truth: Insights are everywhere, but execution is not

Financial institutions today operate on a powerful analytics backbone:

- Credit models estimate probability of default

- Fraud systems detect anomalies in real time

- Marketing models predict customer intent and behavior

- Wealth platforms forecast engagement and portfolio trends

These systems produce sophisticated outputs (risk scores, alerts, forecasts) but they are typically delivered through dashboards, reports, or alerts.

From there, the process slows down. An analyst interprets the data. A business team decides what to do. Operations teams execute the action.

Each step introduces delay, dependency, and inconsistency.

In a world where customers expect instant loan approvals, real-time fraud protection, and hyper-personalized experiences, this raises an uncomfortable question: Why are we still relying on fragmented, manual workflows after generating real-time insights?

The problem: The last-mile gap

The gap between insight and action is where the real inefficiency lies. An insight does not equate to a decision, and a decision does not equate to action.

Insight ≠ Decision | Decision ≠ Action

In financial services, this gap has tangible consequences:

- A fraudulent transaction is flagged but not blocked in time

- A high-value customer shows churn signals but no immediate outreach follows

- A qualified borrower waits hours or days for approval

Even the most accurate prediction loses value if action is delayed. This “last-mile gap” creates:

- Latency in time-sensitive decisions

- Dependency on analysts and operations teams

- Inconsistent decisioning across channels

- Missed revenue opportunities due to slow response

The industry has optimized for prediction but not for action.

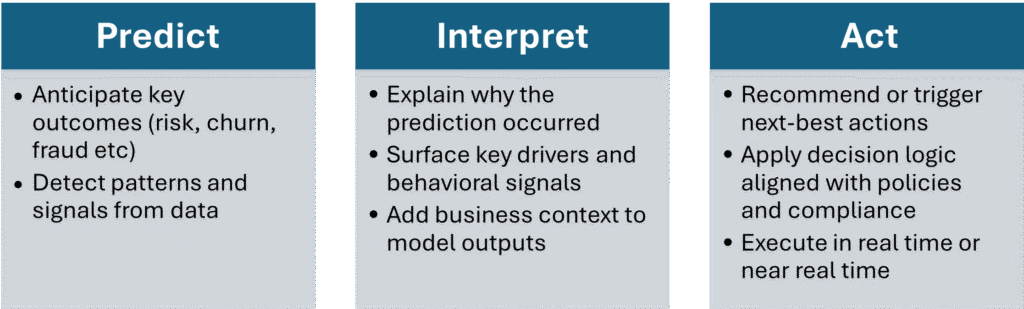

The shift: Agentic predictive analytics

What if a system didn’t just tell you what will happen but also what to do next, and execute it? Agentic Predictive Analytics closes this gap by transforming analytics into a continuous loop of predict → interpret → act

What does this look like in practice?

- A suspicious transaction isn’t just flagged, it’s automatically blocked or verified

- A customer at risk of churn receives a timely, personalized retention offer

- A loan application is instantly approved, declined, or routed

- A cross-sell opportunity is acted on in the moment not days later

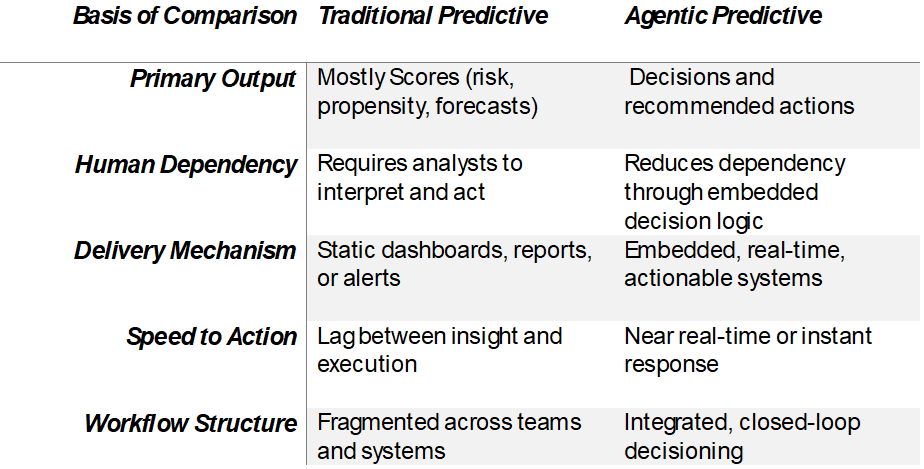

The shift from traditional predictive to agentic systems is not incremental, it’s structural:

When action becomes embedded within analytics, the impact is immediate:

- Faster decision cycles

- 20–30% improvement in conversion rates in AI-driven banking use cases

- Reduced operational costs through automation

- Consistent, scalable decision-making across channels

This data and analytics ecosystem is undergoing a natural evolution – from building models that inform decisions to systems that actively participate in them.

In financial services, prediction is no longer the differentiator. The real advantage lies in closing the gap between insight and action, ensuring every prediction leads to a decision, and every decision leads to execution.

If you want to stay ahead in this evolution of analytics with agentic predictive analytics, connect with AiVantage today.